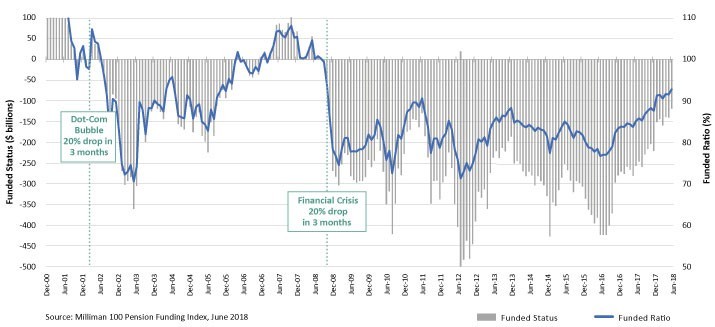

Many CFOs and treasurers have recently fully funded their defined benefit (DB) pension plan. Some took advantage of the larger tax deduction available for 2017 contributions. Others have benefited from rising interest rates and favorable investment returns. However you accomplished it, congratulations! But the real question is: What now? Should you maintain your current asset allocation and hope there won't be another major market downturn, or take action to lock in your fully funded status no matter how markets perform?

The Importance of Locking In Funded Status

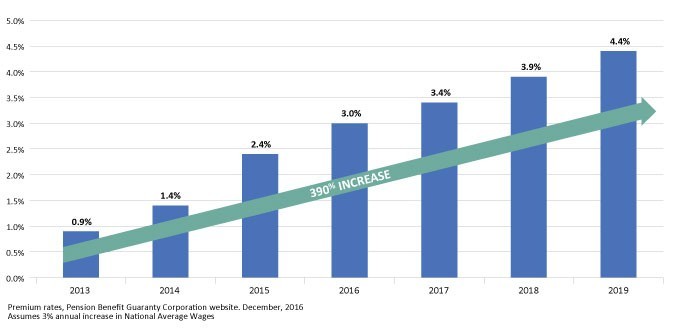

Most CFOs and treasurers would agree that maintaining their plan's funded status is an important goal. The last thing a financial officer wants is to explain to the board of directors why the funded status of the plan has decreased again due to an interest-rate decline or equity market correction. Remember, too, that your underfunded pension plan required you to make additional contributions and pay increasing variable Pension Benefit Guaranty Corporation (PBGC) premiums. Those premiums equal 3.8% of the plan's unfunded liability for 2018 and will rise to at least 4.2% in future years.

So, what kind of strategy can you use to avoid these potential problems? A pension buy-in may be the answer. A pension buy-in annuity contract is a well-tested idea that has been used for many years in the U.K., but has only become available in the U.S. in the last few years.

Increasing Pension Benefit Guarantee Corporation Premiums

The buy-in transfers all the pension risk associated with the DB plan liability for those participants covered under the buy-in contract. To complete the contract, the plan sponsor makes a one-time payment to the insurance company. Thereafter, the insurance company pays a monthly lump sum to the DB pension plan equal to the exact amount of benefits due to those plan participants who are still alive and receiving benefits. The pension plan uses this money to continue making individual payments to its participants.

The buy-in contract remains an asset of the plan, and the insurance company provides a monthly contract statement to the plan sponsor for accounting purposes. This means the liability and assets remain on the plan sponsor's balance sheet, but the funded status will remain stable regardless of how long participants live or what happens with the stock market or interest rates.

Flexibility for Plan Sponsors

With Pacific Secured Buy-In®, the plan sponsor can continue the contract for as long as needed and the plan sponsor remains in control. The contract also can be converted to a buy-out contract at any time for no additional fee. For example, let's say a plan sponsor has just started the plan termination process but will not be ready to complete that process for six to 18 months. With Pacific Secured Buy-In, the plan sponsor doesn't have to worry about what happens to the market or interest rates during this period.

Most plan sponsors will want to convert the buy-in to a buy-out within a few years. This is because, with a buy-in contract, the liability remains on the plan sponsor's balance sheet. Thus, the plan sponsor is still paying all administrative expenses for maintaining the plan. For example, even though Pacific Secured Buy-In can help keep the plan fully funded and help reduce or eliminate future variable PBGC premiums, the plan sponsor still has to pay the fixed per-participant PBGC premiums each year, which will be $80 per participant in 2019.

No Settlement at Buy-In

An important feature of Pacific Secured Buy-In is that it does not trigger the pension settlement accounting transaction while the buy-in is active. Thus, at implementation of the buy-in contract, the company need not recognize in income the unrecognized pension loss it currently has on its balance sheet. With a buy-out, all or a portion of the loss would have to be recognized immediately. For U.S. companies, any pension loss would typically be recognized in income in the year the buy-in is converted to a buy-out. The plan can be terminated when it is most advantageous to the company.

A Bonus for Multinational Companies

In addition to all the advantages discussed thus far, Pacific Secured Buy-In offers an additional advantage for multinational companies operating under International Financial Reporting Standards (IFRS) accounting. Under IFRS, not only is any pension loss not recognized in income at the time of the buy-in, but it also may not be recognized in income upon conversion to a buy-out. A company that did not use a buy-in first and, instead, started with a buy-out would have to recognize any pension loss in income in the year the buy-out contract was executed. However, if the company first uses a buy-in and later converts to a buy-out, the pension loss may never be reflected in income. The buy-in transition will simply be accounted for as a balance-sheet adjustment. This makes Pacific Secured Buy-In an important consideration for any multinational company considering a pension risk-transfer transaction for a U.S. pension plan.

A Strategy to Help Secure Your Funding Level

How stable are your pension-plan investments? By transferring your plan assets to an insurance company through a product like Pacific Secured Buy-In, you will no longer have to manage the investment portfolio or worry about the fund balances. Instead, you can manage your business.