How DB pension plan sponsors can solve their "orphaned" DB SERP liabilities

With many corporate defined benefit (DB) plans now closed, frozen or terminated, many of those same plan sponsors may have leftover—i.e. "orphaned"—nonqualified defined benefit supplemental executive retirement plans (SERPs). These nonqualified DB SERPs, which were put in place for the company's executives and typically mirror the benefits of the qualified DB pension plan, are now also likely closed and/or frozen. However, nonqualified DB SERPs are not easily terminated. Pacific Life's Russ Proctor and Marty Menin spoke to PLANSPONSOR about a solution for sponsors of nonqualified DB SERPs—a solution that can help plan sponsors stabilize their balance sheets and solve the investment and mortality risk associated with these nonqualified plan liabilities.

PS: The trend for corporations who have qualified defined benefit pension plans is to de-risk those plans. How does this affect a plan sponsor that also has a related nonqualified DB plan for its executives?

Menin: Those plan sponsors that have closed or frozen their qualified DB plans likely took similar steps for their nonqualified plans. Many plan sponsors may not realize that they can't easily terminate those nonqualified defined benefit SERPs. If they were to terminate them, they have to be very careful to avoid triggering constructive receipt for the executives. This could create negative financial results for both the company and the executives under Internal Revenue Code (IRC) Section 409(A).

PS: So, if a plan sponsor has taken some action to de-risk its qualified DB plan, how does it also de-risk the nonqualified DB SERP?

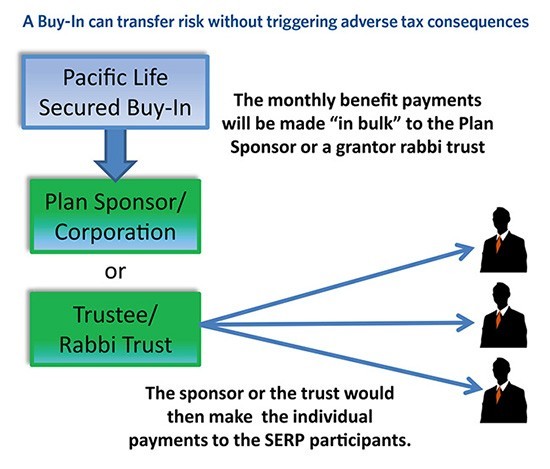

Proctor: The good news is that one of the same solutions used to solve the qualified defined benefit risk can also be used for nonqualified DB SERPs. Our Pacific Secured Buy-In® solution is an asset that's designed to be owned by the corporation or a rabbi trust to de-risk the nonqualified DB SERP liability. With the Buy-In, Pacific Life makes a bulk payment each month to the company or rabbi trust in the exact amount that is needed for the company to make the individual payments directly to the executives.

PS: You're suggesting that a plan sponsor use a Buy-In annuity for its DB SERP liabilities. Could a sponsor use a Buy-Out and be done with it?

Menin: The problem with using a Buy-Out annuity contract is that once the insurance carrier issues an annuity certificate to the executive and starts paying the executive directly, then the executive is in constructive receipt of the full present value of the benefit stream.

PS: Clearly the Buy-In is a better solution. Are there other advantages to using a Buy-In contract as a solution for managing DB SERP risk?