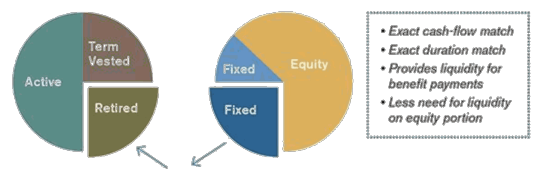

Under GAAP accounting rules, plan sponsors of defined benefit (DB) pension plans must recognize the plan's funding deficit on the company's balance sheet. This wouldn't be so bad if it weren't so difficult to match plan assets to plan liabilities. Unfortunately, DB plans are consistently challenged by volatile interest rates and equity markets. While achieving a precise asset to liability match is difficult in the best of times, it is extremely challenging during periods of volatility.

Many plan sponsors use traditional liability-driven investing (LDI) strategies. However, because the pension payments are paid monthly over a very long period and the pension liability is measured annually based on specific corporate-bond rates, matching assets to liabilities is not an easy task. As those corporate-bond rates move, the liability moves as well. The plan assets not only need to deliver the monthly cash flows to pay benefits, they also have to match the movement in the value of the liability as closely as possible. Traditional best-efforts LDI strategies have had trouble with that precise matching, which results in tracking error.

Asset managers will say to a plan sponsor that they "cannot buy the curve." They're referring to the Citi Pension Discount Curve (CPDC) that's used by many actuaries and plan sponsors to measure plan liabilities. It's a nearly impossible task for an asset manager to buy and hold the same bonds and allocation used to develop the monthly CPDC.

Even if an asset manager could hold all the bonds in the CPDC, it may not be a suitable investment for a pension plan because of the heavy concentration by industry and by issuer of the bonds used in the curve. This concentration increases the downgrade and default risk of the investment portfolio, and thus may not meet the diversification requirements of the plan's investment policy. If a bond is downgraded or defaults during a month, it is simply taken out of the CPDC in the following month. Thus, the CPDC never suffers losses from downgrades or defaults. However, a traditional LDI portfolio that actually purchased those bonds that were later downgraded or defaulted would suffer a loss.