Maybe Annuities Aren't That Expensive After All

Defined benefit (DB) plan sponsors have been contemplating various pension de-risking solutions more seriously than ever. Some plan sponsors have the preconceived idea that annuities are "too expensive." But many plan sponsors have not considered, and have not measured, the true economic cost of their defined benefit pension plans. To further investigate the concept of accounting cost vs. economic cost, Alison Cooke Mintzer, editor-in-chief of PLANSPONSOR, spoke with Russ Proctor and Marty Menin, both directors of institutional sales at Pacific Life. They explained the difference between these two types of costs.

PS: What is a plan sponsor's accounting cost?

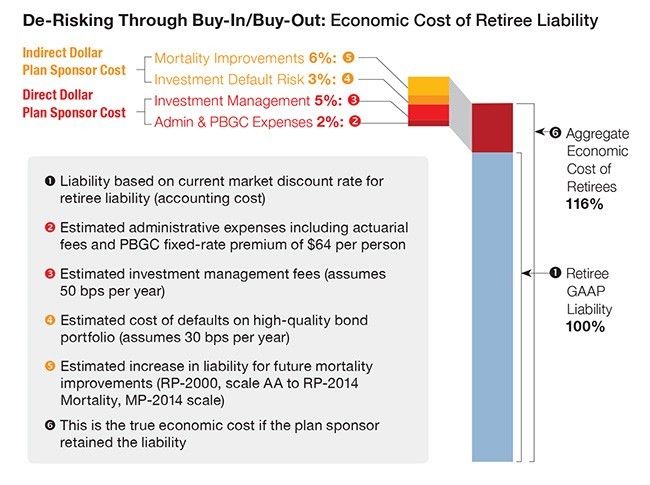

Proctor: Accounting cost refers to the amount of liability the plan sponsor has to report on its balance sheet for its defined benefit (DB) plan. This pension accounting liability is the present value of only the projected benefit payments that the plan sponsor promised to the pension plan participants. It does not include a variety of other direct or indirect expenses that the plan will pay in the future but that the plan sponsor is not required to recognize on the balance sheet now.

PS: What's the difference between that and the economic cost?

Menin: Economic cost refers to the all-in total present value of the costs that the plan sponsor will eventually pay for the maintenance of the pension plan. The direct expenses the plan sponsor pays includes for example: the annual administrative costs, actuarial costs, legal costs, asset management fees and Pension Benefit Guaranty Corp. (PBGC) premiums. Then there are indirect costs for which the plan sponsor may not receive an invoice that need to be recognized as part of the economic costs of the plan.

PS: Can you provide a little more detail about some of those indirect costs?

Proctor: An example of indirect cost is downgrades or defaults on bond investments. If the plan assets are invested in a bond that is downgraded or that defaults, then the plan assets will decrease. However, the plan sponsor does not receive a specific invoice identifying this cost. Another example is mortality improvement. The Society of Actuaries is releasing a new mortality table this year that indicates people are living longer. If participants live longer than expected, then the plan will have to pay benefits for a longer period of time, which will result in additional cost to the plan sponsor. This cost may not be realized in the accounting cost until the plan sponsor updates the mortality assumption. It is expected that the new mortality table could increase the liability 4% to 10%, depending on the age of the participants, compared with the table currently used in determining accounting costs.

Although some of these indirect costs such as default risk and mortality can be quantified and added to the economic costs, others are more difficult for plan sponsors to nail down. For example, there is a cost for the time spent by staff to research questions by participants, search for lost participants, conduct a search for a new asset manager, monitor and reconcile actual and expected investment results, etc. Indirect costs include the amount of time executives spend on all these things that take time away from managing the company's core business. Clearly their time is valuable but nobody is quantifying that expense.

There are many costs that plan sponsors just take for granted as part of operating the pension plan. Accounting rules don't require you to book those on your balance sheet, but you've got to take those into consideration when de-risking and comparing to the annuity costs.